How Do Exchange Rates Work, Anyway?

Folk wisdom, dollar dominance, and hot money

{kind=link}

Before I get to the mechanics of exchange rates and trade—somewhat in the news these days—let me start off with some fortune cookie koans about the nature of Truth:

Lawyers: what’s provable is True.

Artists: what’s authentic is True.

Politicians: what’s popular is True.

Practitioners: what works is True.

Academics: what’s correct is True.

And so on.

By the last of these, I mean that there’s a significant difference between knowledge that can be exhaustively proven to an academic’s satisfaction and what most people are willing to act on in the world.

And there’s probably no topic with greater distance between what academics Know and what the world believes Works than the effects of exchange rate movements on the economy.

Folk Tales of Competitive Devaluation

The practitioner’s view of exchange rates goes something like this.

Let’s imagine two fictional countries: call them Poland and Japan. Imagine the Polish złoty falls in value relative to the Yen. The prices of Polish pierogi and kielbasa are in złoty, so from the perspective of a Japanese consumer, they can buy more kielbasa for the same amount of yen. Poland’s exports to Japan increase. On the other hand, Japan’s exports are listed in Yen; from the perspective of a Polish consumer, umeboshi and sake have become more expensive because of the fall of the złoty. Poland’s imports from Japan decrease.

The folk view of exchange rates concludes that devaluing your exchange rate is good for exports, but bad for imports. Choosing which exchange rate to pursue is thus a matter of political priorities. Historically, developing-country elites from 1950s Taiwan to present-day Senegal have favored overvalued exchange rates, because they like cheaper foreign goods; more recently, fast growers like post-1950s Taiwan and China have favored undervalued exchange rates to promote their exports.

In case this all seems a bit abstract, here’s noted practitioner Donald Trump, laying out the same logic:

So we have a big currency problem because the depth of the currency now in terms of strong dollar/weak yen, weak yuan, is massive… That’s a tremendous burden on our companies that try and sell tractors and other things to other places outside of this country. It’s a tremendous burden . . . I think you’re going to see some very bad things happen in a little while. I’ve been talking to manufacturers, they say we cannot get, nobody wants to buy our product because it’s too expensive.

There’s a whole menagerie of different names for this phenomenon, from “competitive devaluation” to “expenditure switching”. In its crudest form, it’s often reduced to the caricature that a weaker currency boosts GDP by boosting net exports. (This is incorrect as a matter of accounting.) In development, perhaps the most sophisticated perspective comes from Rodrik (2008), who argues that devaluing one’s real exchange rate promotes the relative growth of the tradable sector—which usually means manufacturing.1

But all these views are predicated on the same story, that changing the exchange rate shifts the relative price seen by buyers and sellers, which in turn affects quantities of actual goods in the real economy.

Only problem is—is this actually true?

Exports, Invoices, and Loyalty

One immediate wrinkle is that firms, being firms, can smell a buck to be made. If the złoty falls—in effect, setting an international discount on Polish goods—they may raise their złoty prices a tad, offsetting a bit of the depreciation but allowing them to increase their profits. So some of the exchange rate depreciation is eaten by firms; the “passthrough” to prices observed by importers may be incomplete.

But there’s a deeper issue. With its matrices and subindices and trilemmas, international economics is so complex that one can stumble around a boneheadedly obvious point for years before colliding with it like a mountainside.

To wit: how are prices actually listed?

The chart below, from the IMF’s Boz et al (2022), compiles data on the currencies in which global exports are invoiced:

Around 40% of all global trade is invoiced in US dollars, even though only 10% of global trade is destined for the United States. A similarly large share of world trade (around 46%) is invoiced in the Euro, but this is much more in line with the Euro Area’s share of world trade (37%). Over 80% of global goods and services are thus listed in terms of just these two currencies—and, in particular, 30% of global trade is invoiced in US dollars, even when America is not necessarily involved in the transaction.

This has immediate implications for my little folk tale of Poland and Japan. A hidden assumption behind that story was “producer currency pricing”—that Poland’s exports are listed in złoty while Japan’s are listed in Yen. One could have just as easily imagined the reverse “local currency pricing”, where the importing country’s currency is used—kielbasa priced in Yen, sake priced in złoty. But reality has other ideas. We live instead in a world of dominant currency pricing, where the US dollar reigns.

We can see the consequences first in prices. Here’s a table from Gopinath and Itskhoki (2021), measuring the responses of import prices to exchange rate movements:

Columns 1 and 4 show the conventional view, regressing import prices on just the exchange rate between the two trading countries. Passthrough is not 100%, but it’s pretty high; a 10% decrease in exchange rates is associated with a 7.5% increase in prices. High passthrough, in turn, implies a world operating close to producer currency pricing.

But the moment you control for the movements of the US dollar, as in columns 2 and 5, passthrough disappears: a 10% depreciation in the bilateral exchange rate is associated only with a 1.6% increase in prices. And what’s really striking is what’s going on with the US dollar exchange rate in the third row: a 10% depreciation in the US dollar is associated with a 7.8% increases in prices—even if the US is not involved in the transaction! If not quite a smoking gun, it’s a strong hint that the world we live in is ruled by a dominant currency paradigm.

So much for prices. What does this actually mean for trade volumes—tangible goods and services? Gopinath and Itskhoki (2021) run the same regression as before, but putting trade volumes on the left hand side:

Column 1 here is the conventional wisdom about exchange rates: when a currency depreciates by 10%, trade volumes increase by around 1.2%—not a whole lot, but still a significant positive relationship. But if we control for the US dollar exchange rate, as in column 2, the coefficient shrinks tremendously. Now when the exchange rate depreciates by 10%, trade volumes increase by only 0.3%!

The folk wisdom thus appears to be quite mistaken: exchange rates matter a lot less for trade movements—and, by implication, the real economy—than one might think.

It Was the Practitioners All Along

Careful readers will note that I used non-causal words like “associated” to describe the tables above. Applied microeconomists, who are used to cleaner experimental settings, are usually aghast when they discover the Wuhan wet market that is international macro. The honest truth is that very little in international economics is “exogenous”, since nothing moves on its own. Shifts to global trade flows—including, say, by a 25% tariff on Canadian goods—can be the causes of exchange rate movements, just as often as they are their effects.

Perhaps the best attempt to isolate the effects of exchange rates is a recent working paper by my teachers, Emi Nakamura and Jón Steinsson, with their coauthor Masao Fukui. They observe that countries that peg their currencies to the US dollar are subjected to exchange rate shocks that often have little to do with their local conditions. (As recent experience has shown, the United States doesn’t give much of a damn about what happens to the rest of the world when it sets its policies.) So the differential effect between countries who float and countries who peg—whose currencies are dragged around by the vagaries of the US dollar—gives you a kind of natural experiment for an exchange rate movement.

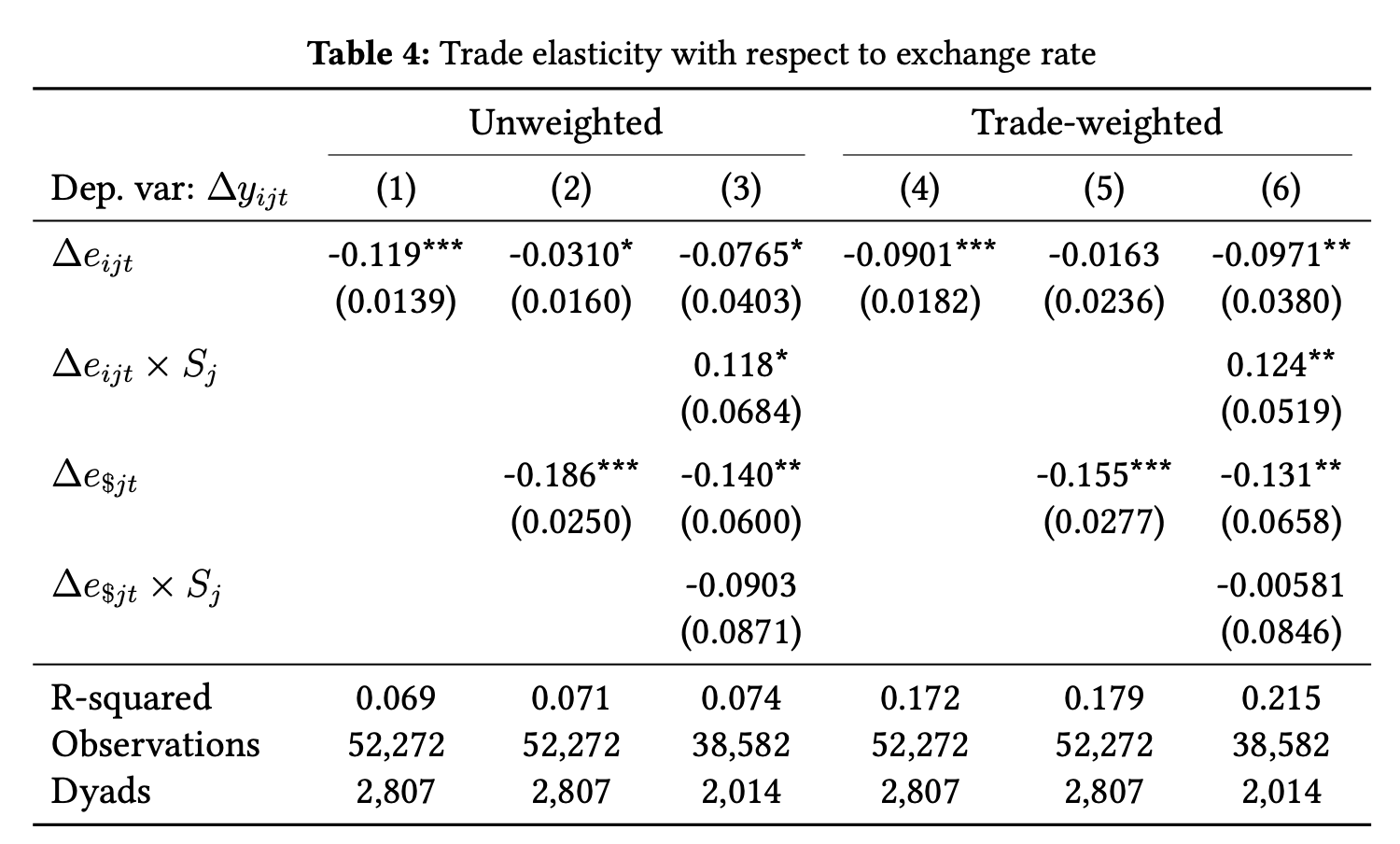

Fukui, Nakamura, and Steinsson then trace the response of several key macro variables to a 1% depreciation of the US dollar. First, the nominal and real exchange rates:

After a 1% depreciation of the US dollar, the nominal and real exchange rates of pegs immediately depreciate relative to the floats (though slightly less than one-to-one, since very few currency pegs are strict). Then, over the following years, the exchange rate slowly starts to appreciate again. So this experiment works— pegged countries have their exchange rates yanked around by the dollar.

Next, macro variables:

The bottom row shows that, just as with the previous table, the response of exports and imports to a depreciation is pretty muted. Exports hardly move at all; imports in the pegs increase by about .3 percentage points of GDP after 3 years. Net exports (exports minus imports) thus fall ever so slightly after a depreciation, by about .3 percentage points of GDP. So far, so good: in a cleaner quasi-experimental setting, we’ve confirmed the Gopinath and Itskhoki result that exchange rates hardly seem to move trade volumes around at all, consistent with dominant currency pricing.

But how can we explain that graph in the top-left: why does investment— typically thought of as a domestic variable—go up because of a currency depreciation?

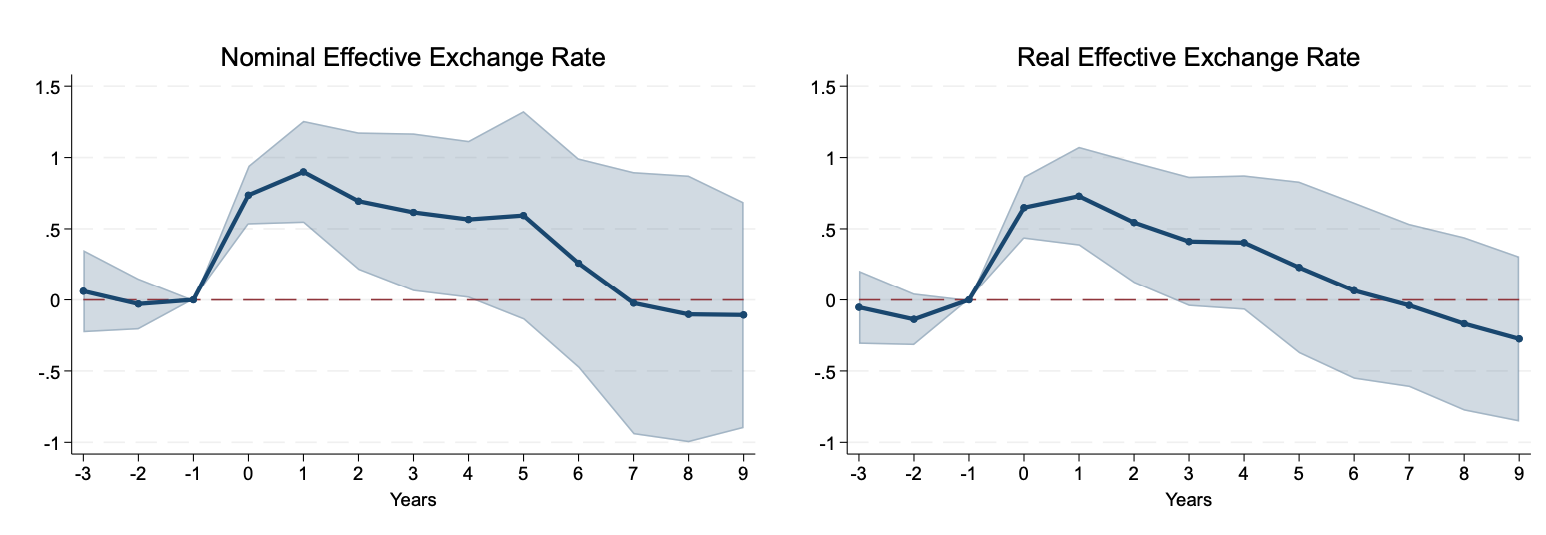

And it’s not just investment—GDP and consumption also increase:

In response to a 1% dollar depreciation, GDP in peg countries rises by around 0.4% after 5 years—quite a large estimated effect for a currency that can move by 10% in the space of a year. In the paper, they find that this is largely driven by growth in the non-tradables services sector, not manufacturing like the Rodrik (2008) view might predict.

We have a strange pattern of results where domestic macro variables appear to respond more to exchange rates than trade itself.

The authors’ answer to the puzzle lies in a market we’ve been studiously ignoring: capital. Applying their methodology to nominal interest rates and inflation, they find (somewhat noisy) evidence that interest rates appear to increase in response to a depreciation:

For currency traders holding assets in a pegged currency, this is a great deal. After the initial shock fall of the exchange rate, the currency slowly and steadily appreciates. Factoring in the (noisy) increase in nominal interest rates, this means an increase in the relative return of assets in the pegged currency. In finance jargon, this violates uncovered interest parity. In plain English, traders smell money.

And this brings us full circle.

Currency depreciations, Fukui, Nakamura, and Steinsson argue, appear to juice the economy by raising the return on assets in the depreciating currency. This brings in the “hot money” from days of yore: global capital flows in and borrowing increases, boosting consumption, investment, and service sector growth. Returning to our fortune cookie wisdom at the top, it may perversely be the Practitioners’ belief that Depreciations Work that actually powers the boom.

What Works Is True turns out to be correct. Just not in the way that anyone intended.

Please consider subscribing to Global Developments to receive more essays on global economics, development, and poverty. Some recent posts:

In 2010, Zambia’s national accounts were assembled by one person. How Much Should We Trust Developing Country GDP?

No, South Korea Was Not Poorer than Kenya in 1960: a quick tour of historical legacies, developmental states, and family history.

The early life of Albert Hirschman—resistance hero and development economist—and his remarkable Strategy of Economic Development

With a little algebra, the real exchange rate works out to be the relative price of tradables to nontradables between countries. Because of sticky prices, Rodrik argues, the nominal exchange rate can effectively set the real exchange rate. A depreciated exchange rate, which effectively subsidizes the tradable sector, can thus encourage the development of tradable goods.

Great read, so basically devaluing a currency boosts non-tradable sectors (like tourism, real estate)and brings in hot money. The conventional theory that devaluation leads to export led growth isn't really that accurate since the strength of devaluation boosting exports isn't that strong. So the idea that devaluation brings growth is right, but people say it for the wrong reasons.

This makes sense because when a country devalues a currency, then that central bank usually tries to increase interest rates to stem inflation. A trader could make easy money by doing carry trade. Borrow in a relatively low interest currency (yen, swiss franc,euro) and buy in a high yield currency that just did a devaluation. We see this all the time with Egypt or Brazil!

Is it possible to distinguish trade that is “really” priced in dollars from trade that uses dollars as a medium of exchange? That is, a non-US company could quote its prices in USD and keep them more or less fixed in USD terms regardless of the local currency’s fluctuations. Or, it could internally price its goods in florins, and then send over invoices in USD based on whatever the florin-dollar rate was at time of purchase. This would presumably save the buyer some hassle while still insulating the seller from exchange rate risk.